Customers are increasingly doing more 'top-up missions' to pick up items in between their main (or 'big') grocery shop – or multiple top-up shops instead of one big shop. On these convenience missions they care about speed and efficiency; making sure they leave the shop with the few items they went for. Expectations of convenience are changing – consumers want more control and less ambiguity from the experience. That means they’re looking for more upfront information before they get to store, and they’re looking online to help them get it. How can digital play a pivotal role to win these 'top-up customers' to store? We conducted this research and Google analysis to find out.

Small baskets, big changes: What it means for retailers

Conducted in partnership with Kantar and Basis, and with further Google analysis, this research demonstrates the changing meaning of ‘local’ in grocery top-up missions. Through this work we've been able to better understand the emerging role of digital and how it is impacting behaviours in store. It also revealed new opportunities for grocery brands to use digital to deliver store sales and acquire new customers.

The evolving grocery sector

Over the last decade, the grocery sector has been in a state of change and it’s set to continue evolving in the coming years. These changes will have a significant impact on the future commercial success of grocers.

We’ve seen net margins more than halved, the rapid growth of discounter brands, the evolution of online grocery shopping (with the U.K. market being the most mature), and disruption from online players like Amazon, meal-kit businesses, and home delivery services.

All of this has changed the market dynamic significantly – but of course, it’s also impacted consumer journeys and the ways we want to shop.

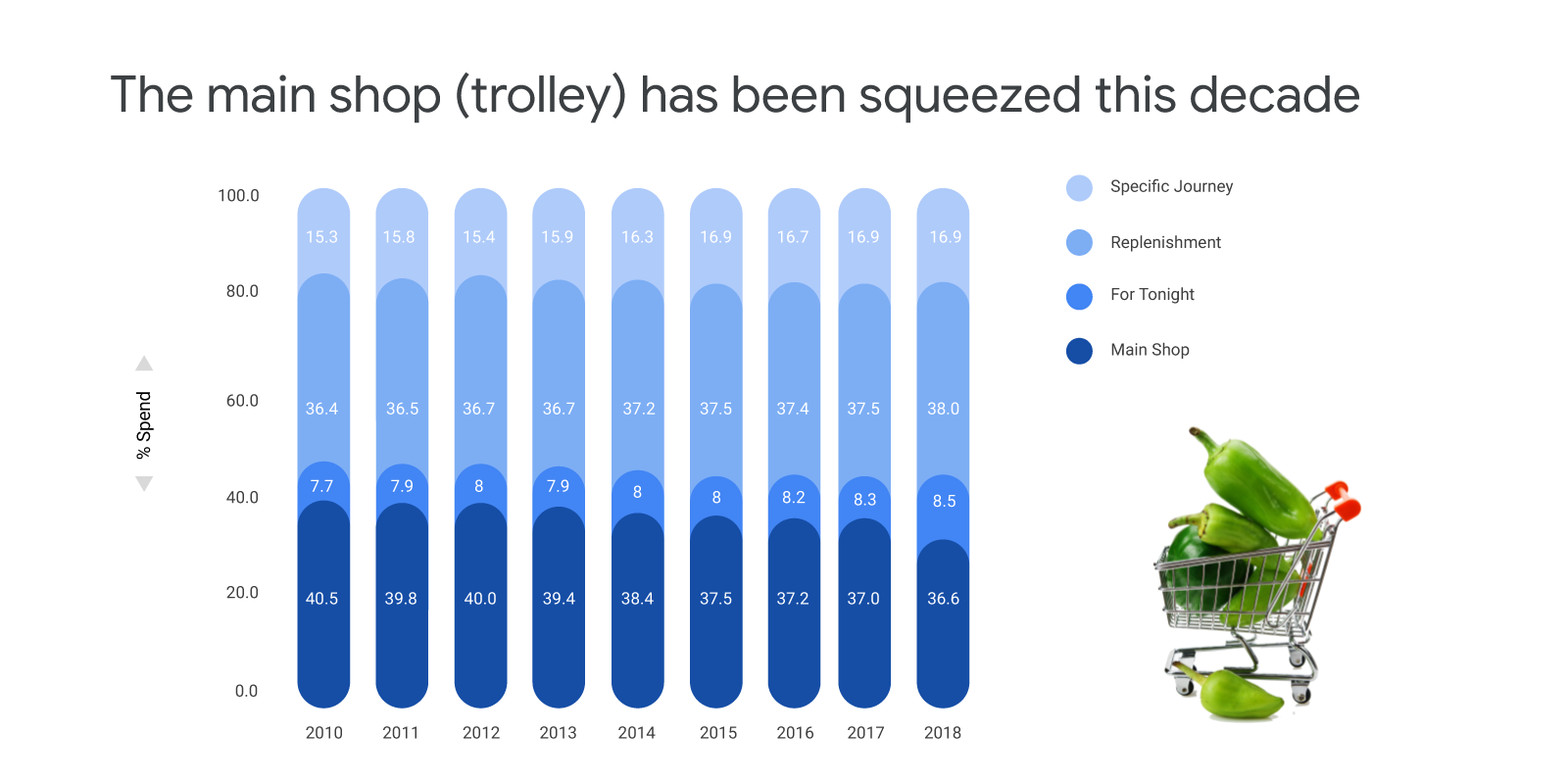

Every year consumers are doing increasing numbers of top-up missions and as a result, reducing the number of main shops they do. We can see the shift in how we shop demonstrated in the Kantar data below. Top-up missions in 2018 accounted for 63% of missions compared to 59% in 20101:

We know that these convenience customers are potentially the easiest to win. From our work with Kantar, we saw that 50% of consumers on convenience missions have weak loyalty to the supermarket brands they use. Additionally, 41% of customers who had done a top-up mission the week before told us they could have chosen a different store than the one they ended up going to.2 These trips are disruptable – consumers are more flexible with store choice than they are on a main shop. We also know that digital is playing an increasing role in meeting new consumer needs and is impacting which store they go on to choose.

To dive deeper, we wanted to answer a key question for retail marketers – what is the role of digital in driving in-store top-up-shopping behaviours and what are the digital levers we should be using to affect them?

Digital is playing an increasingly important role in meeting consumer needs and often influences the store they choose.

The research

We developed a three-phased research and analysis programme to answer this question from different angles while ensuring the customer and their needs were at the heart of our work.

- In partnership with Kantar, we did some quantitative work to understand claimed behaviours at a nationally representative scale. We spoke to thousands of consumers who had completed a top-up mission the week before to understand what role they felt digital was currently playing or could play in their future trips.

- Then, in partnership with Basis, we followed up with a piece of mobile ethnography, where we closely observed consumer behaviours for a week. We were able to see what respondents did on their mobiles, what they went on to do in-store, and what their frustrations and needs were.

- We looked at Search and Maps data to explore store-focused intent (e.g. ‘grocery brand name’ + ‘location’). This helped us uncover insights about digital demand to grocery stores and the growing role of Search and Maps in grocery-store missions.

What we found out and the opportunity for grocery brands

A key theme that emerged from our research was the issue of risk for customers on top-up-missions. Respondents told us that when they go shopping for only a few items they feel disproportionately disappointed if their trip-to-store resulted in not getting the item they wanted or not getting it at a price they expected. This is different to how they feel about the main shop, where they know that making substitutions is a normal part of the experience.

Consumers’ expectations of convenience are evolving and are being shaped outside the grocery category. They expect that digital should be a key tool for them in managing risk but the reality of the experience often lets them down. Why?

They’re comfortable with the digital ‘basics’ like searching for directions, opening times, and store facilities – but, this is largely because when they search for those things the information is readily available. When they try to use digital to meet their more pertinent needs (in-stock availability, pricing information) they are often left frustrated.

The key frustrations consumers encounter:

- The online experience doesn’t match what’s in-store (i.e. inconsistent pricing or range information)

- Poor online user experience means they can’t find what they’re looking for (e.g. being directed to recipe inspiration rather than stock information)

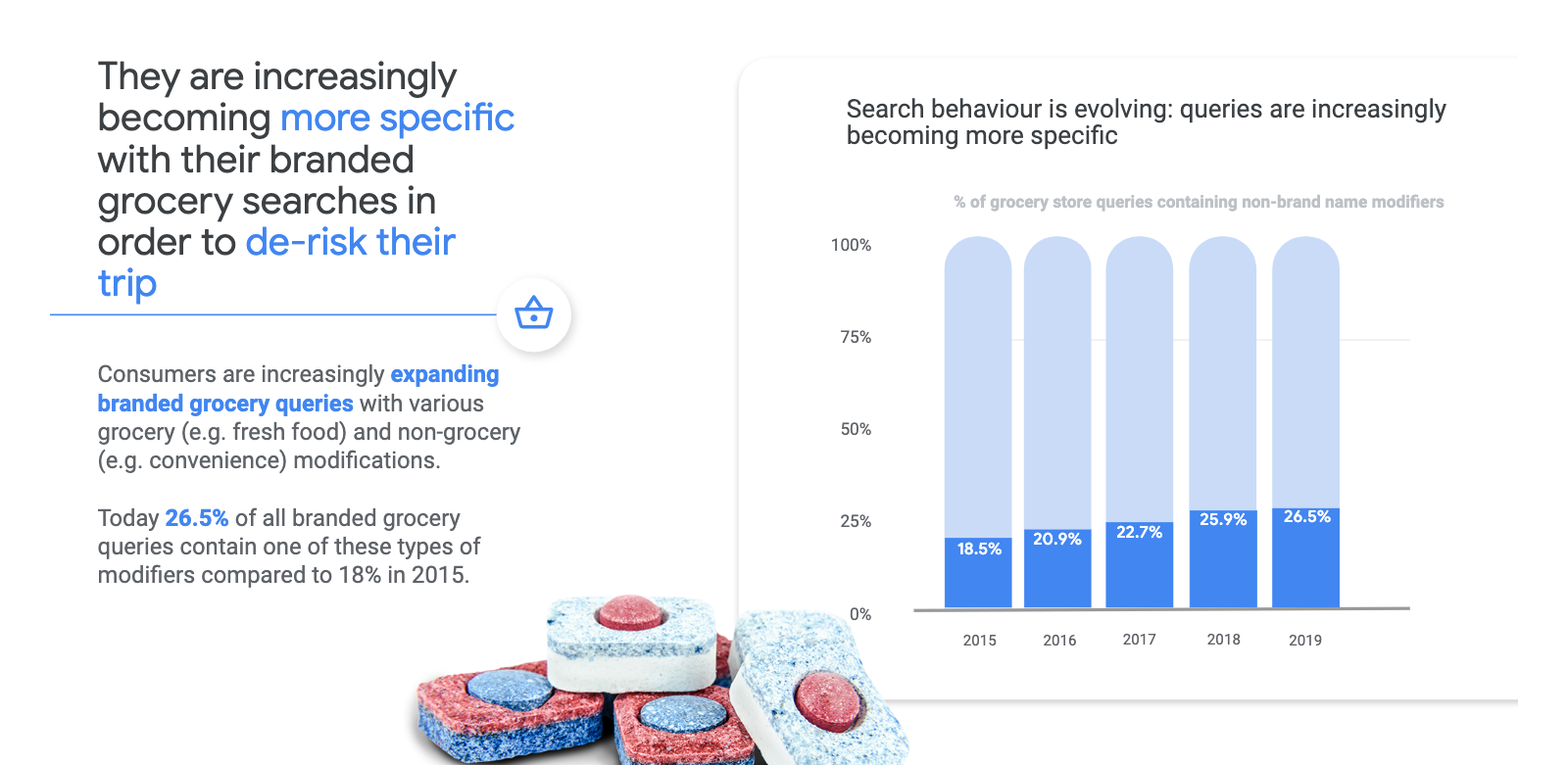

In this context, we see consumers becoming ever more specific when they do grocery-related searching. We see searches for specific stores increasing every year, and we see consumers using more specific terms related to grocery brands to help them get to more definitive answers.

What are the key needs we saw consumers trying to address with the help of digital – and what can grocery brands do to help them?

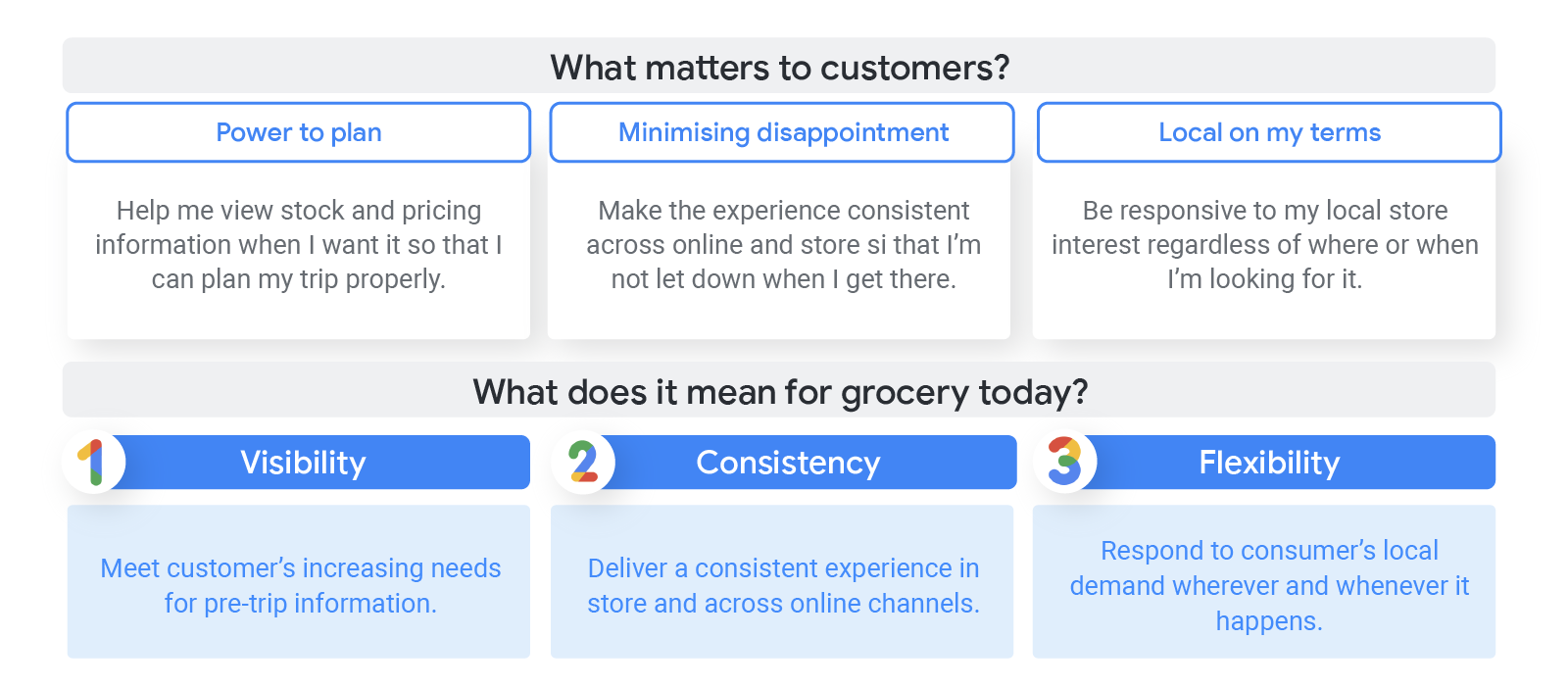

1. Minimising disappointment

Consumers want to increase control and reduce ambiguity when it comes to convenience. They don’t want nasty surprises when they get to a store and want the process to be as easy as possible.

“Unfortunately, the variety pack I had seen online was sold out so I was forced to purchase the “lightly salted” multipack instead. This was somewhat annoying as I had my mind set on the variety multipack,”3 said one respondent.

Look at Google My Business for inspiration – it’s a digital front window for stores – and allows retailers to showcase the type of information that will drive shoppers to their stores. Retailers can do things like upload photos, share offers, and create events to help their business stand out to potential customers.

2. Power to plan

Consumers are researching for convenience grocery missions, largely to minimise risk of disappointment. They told us in both the quantitative and qualitative research that they want more visibility of what’s in-stock in-store (products, ranges, brands), and want to be able to see a consistent price from online to in-store.

- 48% of consumers said they would like to be able to see pricing and promotion information before they went to store

- 29% said they’d like to see products stocked by store4

Consumers expressed their frustration with inconsistency between digital and physical channels. This carries risk for brands. We appreciate how difficult it is for grocers to address this – the high volume of SKUs, and frequency of shopping trips, makes it extremely challenging to accurately share live product information. But, it’s something to think about.

That said, we’re starting to see grocers follow general merchandise retailers’ leads in having success with Local Inventory Ads on Shopping campaigns.

Consumers want control on their convenience journeys; giving them the power to see where the product is in-stock near them enables them to gain this control, and decide on which mission will be truly most convenient for them.

3. Local on my terms

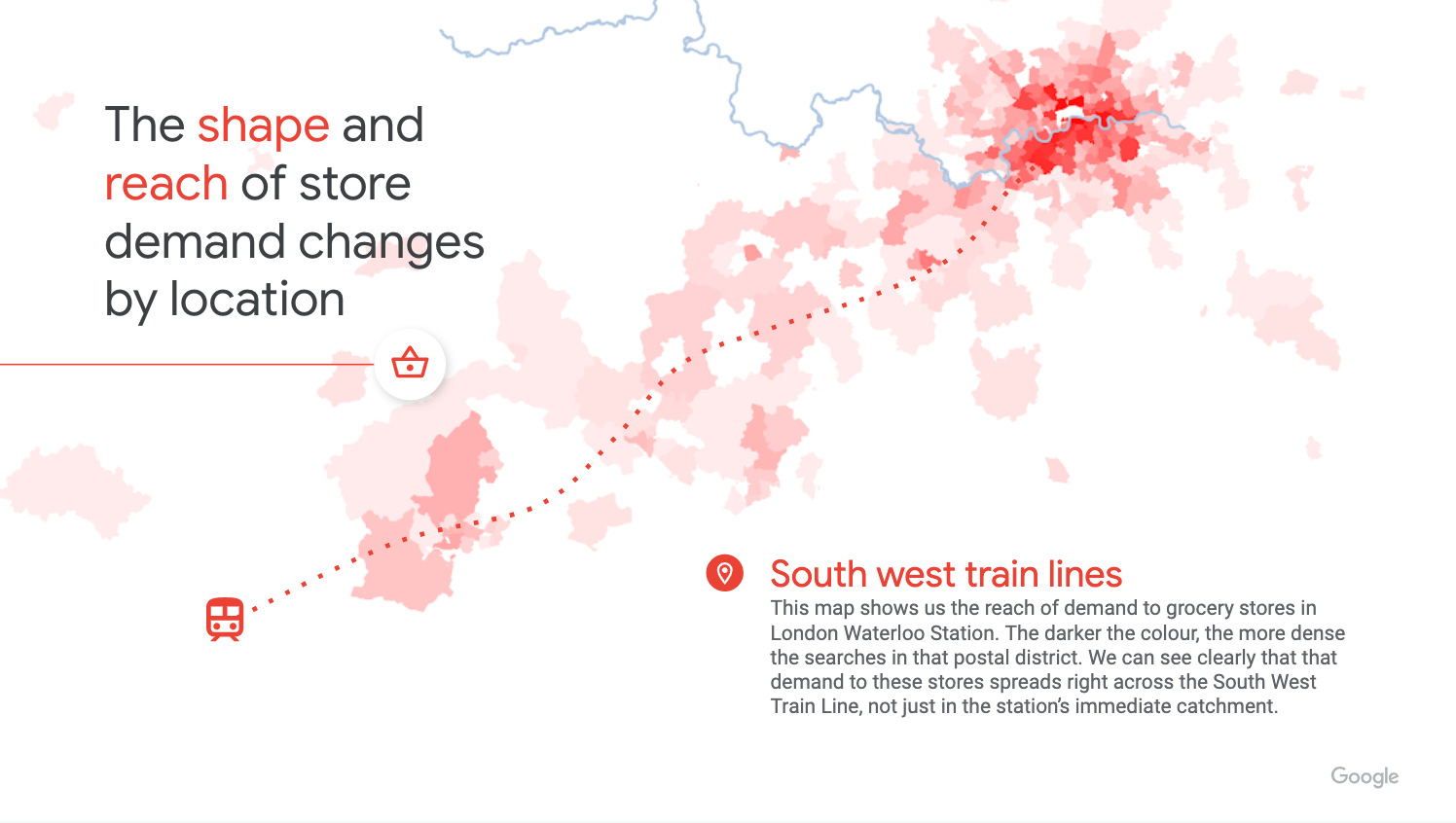

From our analysis on store-focused searches, we saw the scale and complexity of online demand to stores. In fact, each store has its own demand dynamic. We saw that local demand online may not actually behave locally, in fact, the average digital store catchment area was 13.4km5. These demand dynamics change depending on a number of factors including time of day, day of week, store format, brand, and region.

We uncovered some surprising insights at a national level too. For example, 31% of searches for grocery stores in central London come from outside the area, and 60% of searches for grocery stores in Brighton come from outside the area6. Consumers are imposing their own conditions of ‘local’ and ‘convenience’ onto stores, stores that may in fact not be in close physical proximity.

We created a number of visualisations to demonstrate how demand to stores behave online. Here’s an example of how volume of searches to grocery stores in London’s Waterloo station spread across the South West train line:

Local Campaigns can help maximise footfall to your stores.

Local Campaigns finds the right shopper across any one of our platforms (Maps, Search, Google Display Network) by engaging with shoppers who are most likely to visit the store. It delivers the right message wherever the shopper is researching and shopping (across Search, Maps, YouTube, Display) because of its ability to understand the context. This means that we can gather a number of factors; the query term, past and present user location, distance to store, shopper device. You can use Machine Learning to interpret what matters most to a customer and deliver the most effective creative, format, and message with the aim of driving that customer to store.

In summary: What retailers should be thinking about

Digital is now a core part of most grocery shopping journeys, especially in certain top-up missions. Consumers' expectations of what digital should do for them in their grocery shopping experience is, thus far, ahead of the reality, and this is leaving them frustrated and disappointed.

There is a big opportunity to win shoppers and drive loyalty if retailers can:

- Help customers meet their increasing need for pre-trip information

- Deliver a consistent experience across channels; digital and physical

- Respond to consumers local demand on their terms