- Consumers are increasingly searching for financial products online and on their mobile devices.

- Banks can provide a holistic, omni-channel banking experience by using data and machine learning to deliver on three core strategies: loyalty & cross-sell, audience engagement, and omni-channel.

- Banks can achieve data-centricity by unlocking silos, determining customers’ lifetime value (LTV), measuring attribution, and getting smarter at buying.

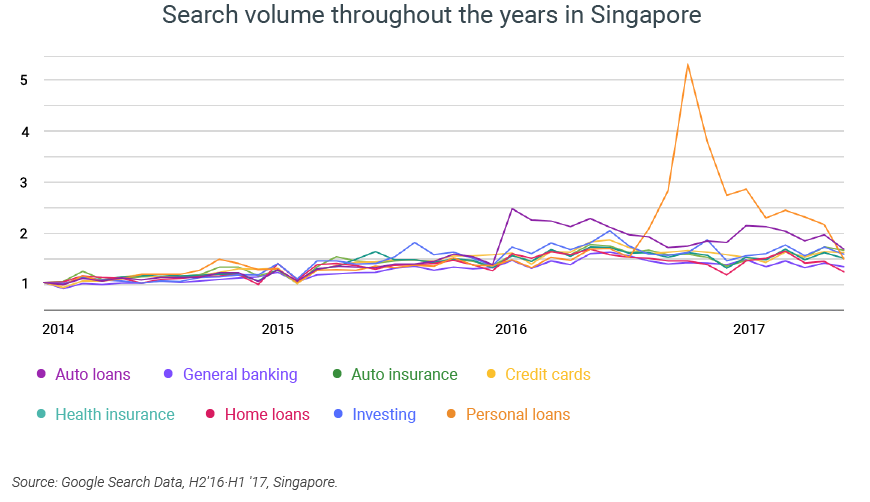

Over the last three years, searches for banking products like credit cards and personal loans have been steadily increasing. Singaporeans searched for personal loans 84% more than they did before, while interest in credit cards in the Philippines increased by 31%.1

In Australia and India, 80% and 89% of searches related to financial services are related to these categories.1 Across APAC, more and more consumers are using their mobile phones not only to research what banks have to offer but also how to educate themselves when it comes to money. In fact, “how to invest money” and “what is a mutual fund” are among the top mobile searches in India, while Australians are using their smartphones to help them plan for home loans.

Despite this trend toward digitization, many APAC banks have yet to take full advantage of new tools and technology that can help them make the most of digital data and measure its true impact on consumers. The learning curve has been slow, with only a few banks championing the different roles digital can play throughout the customer journey.

Keeping in mind the differences between simpler products that can be fulfilled online (credit cards, personal loans, etc.) and traditional retail-based products like wealth management and insurance that require higher touchpoints, APAC banks can provide a more holistic, omni-channel banking experience by unifying data to achieve a clear view of the consumer. Keep reading to learn how some of the world’s best data-centric companies use data and machine learning and ultimately determine where your company stands on the path to data centricity.

Understand the full value of data

The journey to data-centric marketing starts by understanding the full value of data. Data can help you achieve a full view of digital’s impact on your bottom line and develop omni-banking marketing strategies across all channels. We’ve found that best-in-class companies use data to power these three core strategies in their businesses:

Loyalty & cross-sell

When customer product data is seamlessly integrated into a remarketing strategy, brands can not only keep existing customers loyal but also cross-sell to current customers across digital platforms—a strategy that is far more cost-effective in generating sales than trying to acquire new customers.

Audience engagement

First- and third-party customer data can help power and optimize brands’ campaign targeting. By learning what audiences are engaging with and searching for, brands can develop customized creative and serve highly personalized messages to the right users at the right time.

Omni-channel

Messages crafted for traditional media channels should be different than those created for digital, but that doesn’t mean brands shouldn’t integrate non-digital data (ATL, BTL, retail, ATMs, etc.) into their targeting. For example, beauty giant Sephora used loyalty card data to determine whether its digital campaigns were influencing offline sales.

Machine learning tools like store visit conversions can help determine the number of users who clicked on a search ad and then visited a physical store by matching users’ aggregated, anonymized location histories with hundreds of first-party location signals. Marketers can then optimize their digital campaigns by device type, location, and specific keyword or product category proven to drive the most customers into stores.

Analyze and identify barriers to data-centric success

The vast amount of data available to marketers today is exciting, but it’s not being used fully if you’re unable to yield insights from it. By integrating data strategy, teams, and technology, APAC banks have an opportunity to make better marketing decisions. While strategies will vary based on business goals, below are four key hurdles to overcome in order to successfully achieve data-centric marketing:

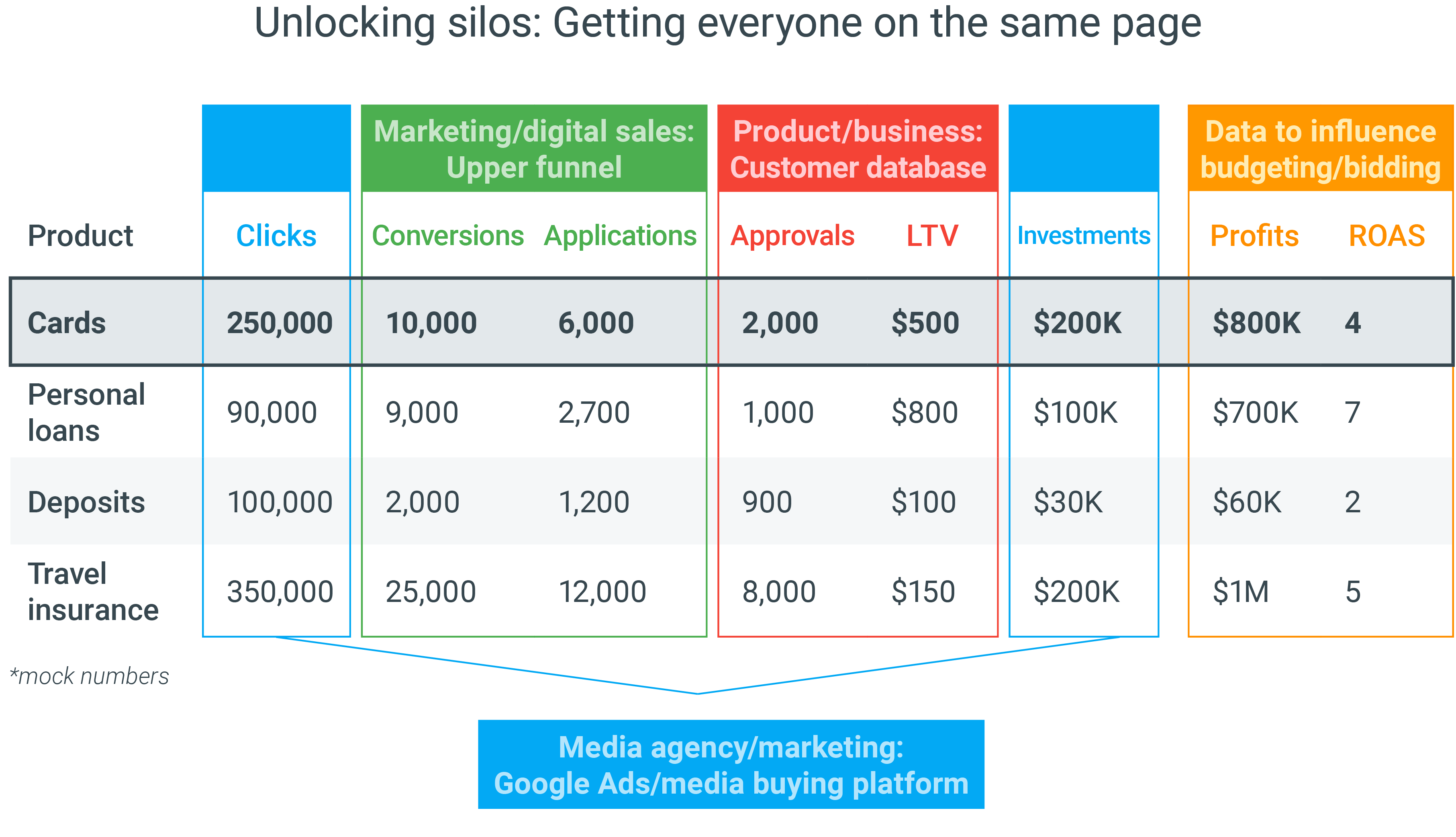

Unlocking silos

Most APAC banks still look at internal data, external data, and intent signals in silos. When data is looked at together holistically, banks can gain insights into a consumer’s full purchase journey and long-term relationship with the bank—from opening a checking or savings account to getting a credit card or housing loan to even planning for retirement.

For example, let’s say a bank’s media agency is given a budget and sets a bidding strategy on a media buying platform. The agency is also tasked with a getting a target number of clicks on an ad (250,000). The marketing/digital sales team then captures the number of users who have successfully converted from the initial click (10,000) and successfully completed a credit card application form (6,000). Of the 6,000 applications, the product/business team approves only 2,000 applications and knows the average LTV of a credit card applicant is $500, resulting in $1,000,000 in net revenue. After deducting the bank’s initial campaign investment of $200,000 to acquire new credit card customers, the campaign yielded $800,000 in profits, signifying a 4X return on ad spend (ROAS). However, if the bank unified its data sources, it would see that personal loans actually generated a higher ROAS (a return of 7X), and it should therefore increase its ad spend budget around its most profitable product.

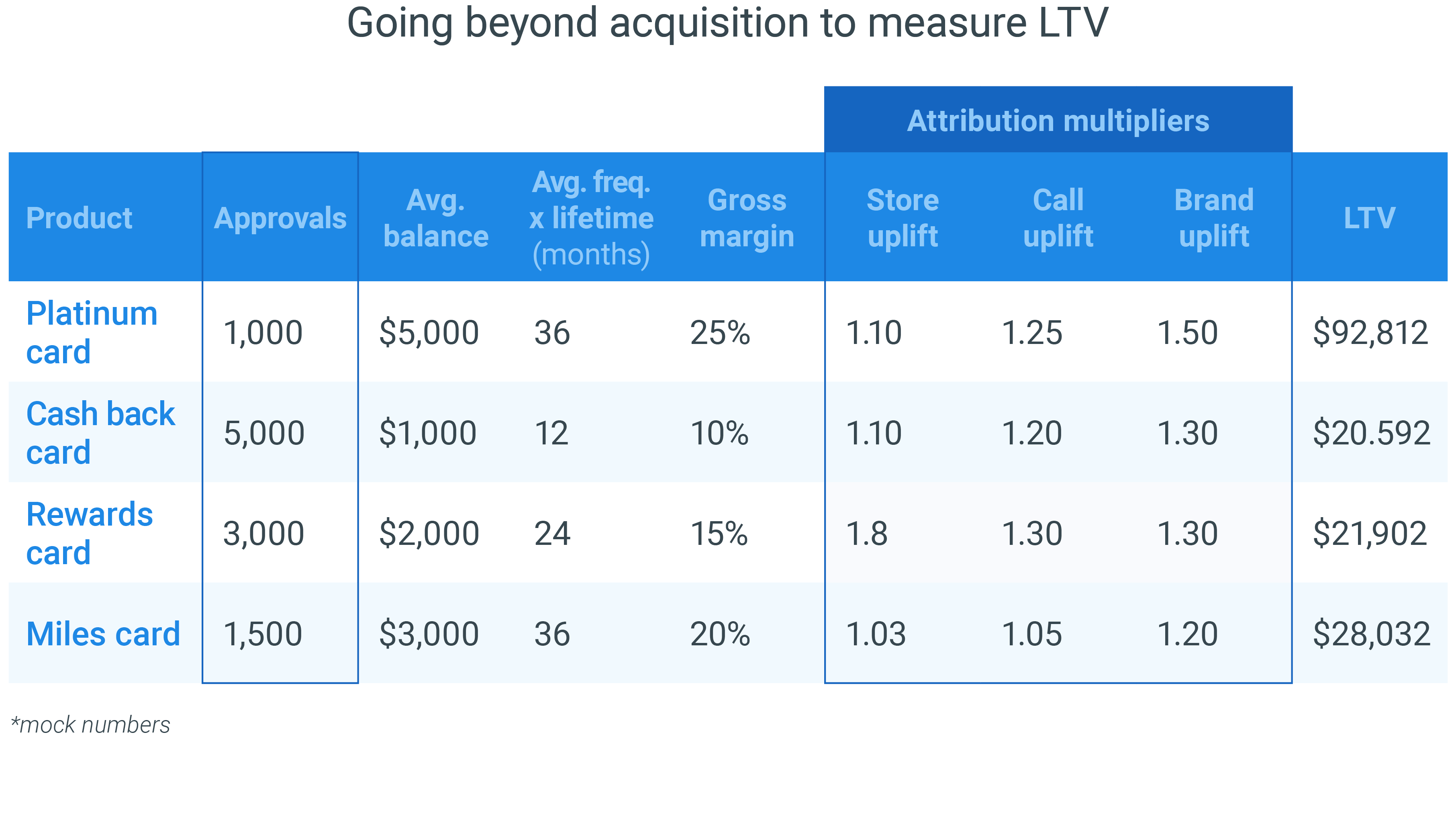

Determining LTV

Instead of focusing on one-time sales or cost-per metrics, APAC banks need to determine who their most valuable consumers are and create the best, most holistic experiences for them. When different products that are tailored for different valued conversions are no longer treated the same, banks will see increased ROAS.

For example, while it may be more expensive to acquire a platinum card user, the chart above shows that the LTV of a platinum cardholder is ~4.5X higher than that of basic credit card user. What’s more, the bank can cross-sell life insurance, retirement plans, and wealth management services (measured by multiplier “uplifts” to in-store traffic, call center conversions, or brand value when their data is upsold to various other acquisition channels) to platinum users, making them a better investment.

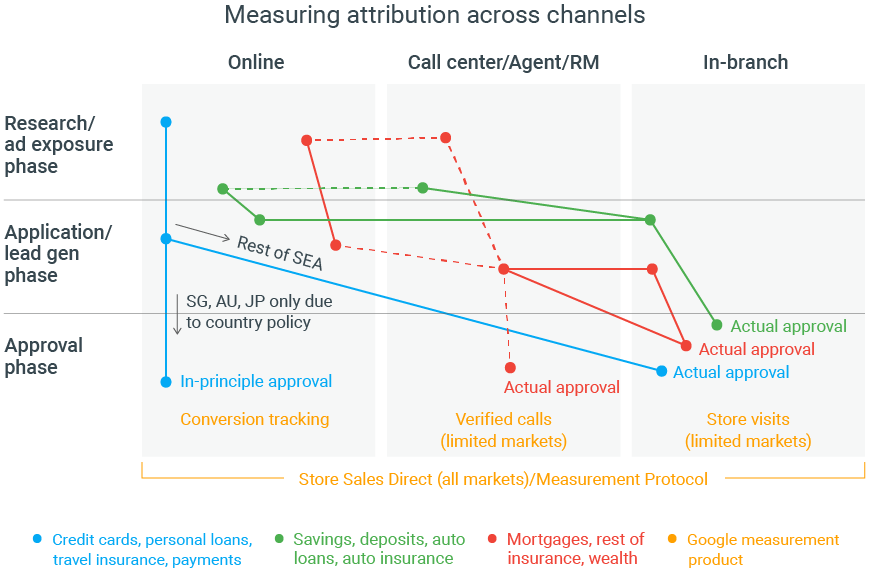

Measuring attribution

While key products like credit cards, travel insurance, and personal loans are mostly fulfilled online, lower frequency and higher barrier to entry products like mortgages, insurance, and wealth management often involve multiple touchpoints as consumers research and fill out applications online and are qualified by call center agents or relationship managers before finally getting in-branch approval. To better move potential customers down the purchase funnel, banks need to use technology that can help them measure the full impact of all stages of the purchase journey.

For example, research, application, and in-principle approval for low-touch products like credit cards and personal loans can all be completed online in Singapore, Australia, and Japan. But for other markets in Southeast Asia, users that are served ads online still have to visit a bank’s physical location to complete an application. In this case, a branch manager may take credit for the conversion without giving proper attribution to the digital interaction in the upper funnel.

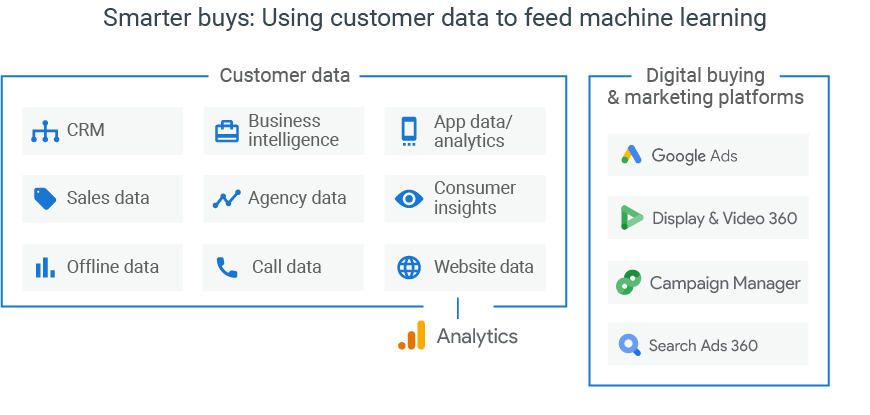

Buying smarter

The wealth of APAC banks’ CRM and third-party audience data is purchased from major credit card companies and other research providers and isolated from their digital marketing teams. However, Google Ads2 and Google Marketing Platform3 allow marketers to look at audience data and analytics holistically and consolidate media buys on a single platform. Tools like Measurement Protocol allow banks to send data to analytics from any internet-connected kiosk or ATM, while store sales conversions can help banks match offline transactions with ad clicks.

How APAC banks can take action

Are you properly using data and machine learning to track and measure sales, margins, and investments across channels and platforms? Download the deck below to kick off a conversation with your marketing team, partner agency, business intelligence analyst, or product team.