A once-in-a-generation shift is taking place in the personal finance space in the Philippines. The shutdown of physical services during the pandemic compelled people to conduct more financial transactions online. From paying bills to managing investment portfolios, Filipinos now prefer digital finance over offline banking,1 and 80% say they’ll continue to use digital banking post-pandemic.2 For financial brands, this presents a never-before opportunity to meet people’s needs.

To help marketers understand the dramatic shift in Filipinos’ financial consumer behavior, Google, Kantar, and Sixth Factor collaborated on the first-ever qualitative and quantitative study that identifies the factors shaping Filipinos’ financial decisions.

We discovered three banking trends across all audience segments: an eagerness to grow wealth through saving and investing, concern about the safety of digital finance, and the use of Search throughout people’s finance journeys.

Going deeper, our study identified key behaviors and motivations of the different banking segments, from the unbanked, who have no bank account, to the underbanked, who have some but insufficient financial coverage, and the banked, who are fully covered.

Here, we share key consumer insights on the different banking segments to help brands better meet their audience needs. First, the three banking trends that hold across all banking segments:

1. Filipinos enjoy digital convenience but safety concerns remain

Filipinos are drawn to the convenience of digital banking,3 but safety concerns hold many of them back. Four in 10 Filipinos believe online banking is unsafe, even though increased access to digital finance services has helped people realize online banking is safer than once assumed.

Brands can increase Filipinos’ confidence in digital finance through education and user-friendly platform design. A simple customer journey will help brands reach people who are new to digital finance. Detailed onboarding and tutorials on how to use financial products, such as e-wallets and finance apps, will help people feel comfortable using them more frequently.

2. Filipinos turn to Search during their finance journey

Whether they’re looking up financial services, reviews, or advice, Filipinos turn to Search as they explore, evaluate, and validate information. Brands should therefore be present on Search and guide people to the right financial information, so they feel confident about their decision.

3. Filipinos are interested in saving and investing

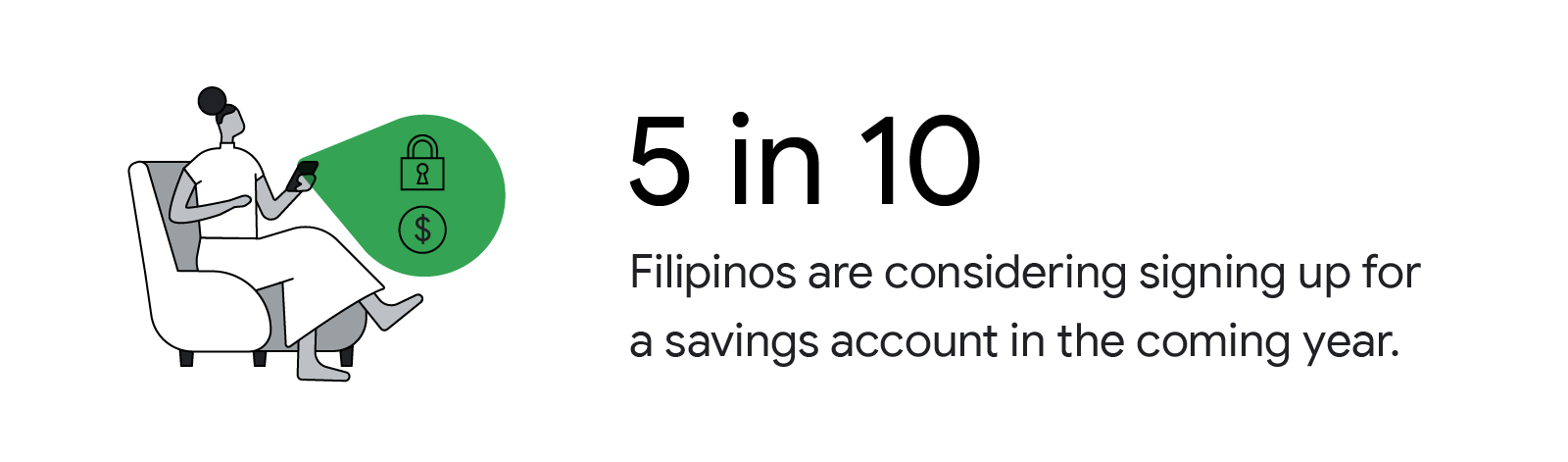

With 50% of Filipinos considering signing up for a savings account in the coming year,4 brands have an opportunity to provide digital finance products that cater to people’s financial needs. Day-to-day online banking activities are especially popular across the board, with 7 in 10 Filipinos accessing e-wallets weekly.5 The more financially savvy members of the banked population are exploring riskier complex investments to grow their wealth.6

Deep dive: Behaviors unique to the banked, underbanked, and unbanked

Although there is an overall shift to digital finance in the Philippines, it plays out differently among the various banking segments. To cater to your audience, it helps if you understand their key motivations and behaviors.

The unbanked need help getting started with digital finance on mobile

The unbanked comprise 71% of the Philippines’ adult population, and many of them are accessing digital finance services for the first time through their phones. Brands have an opportunity to meaningfully reach this new generation of customers if they understand their needs and build a relationship with them early on.

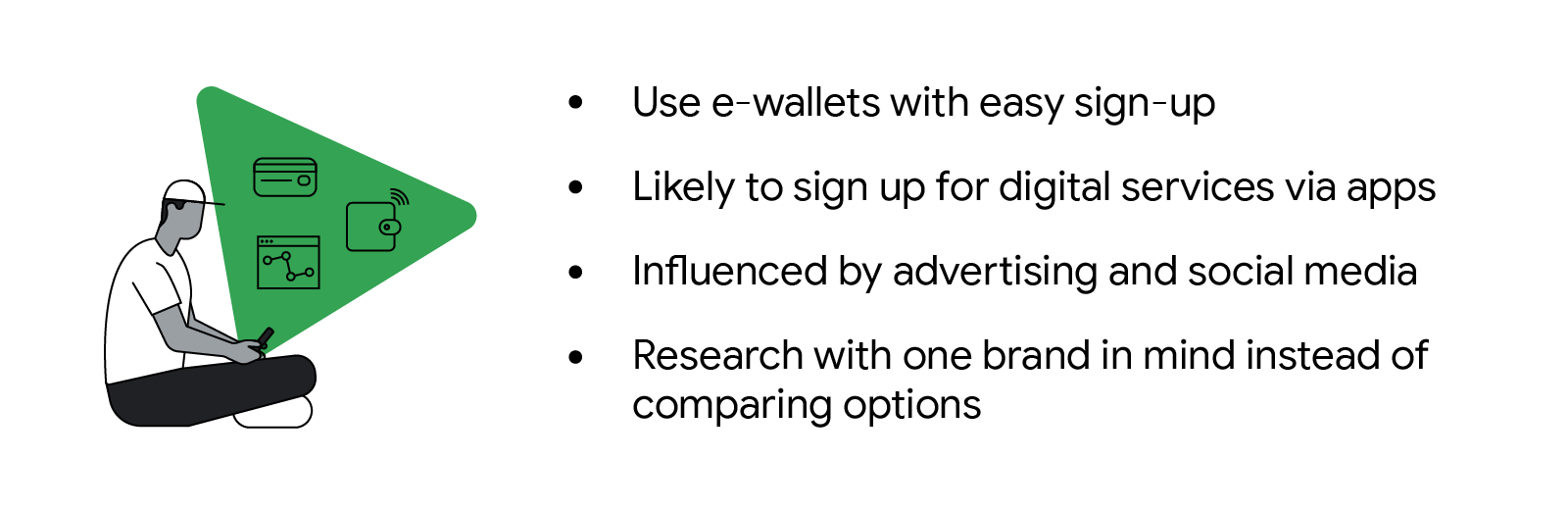

Financial behavior traits of Filipinos in the unbanked segment

Take, for instance, how 78% of the unbanked use a simple e-wallet.7 It’s easy for them to sign up for this digital service via a mobile app,8 and they don’t have to submit many personal documents or maintain a minimum balance. Brands, by showcasing the versatility of e-wallets, such as the fuss-free money transfers it enables, and by promoting its frequent use in everyday transactions, can help the unbanked feel confident about exploring other financial products.

Many in the unbanked segment also have safety concerns about digital financial tools because they’re using them for the first time.9 Brands can build trust by helping people become familiar with these tools, and they can do so via social media and online advertising because the unbanked are influenced by these channels.10 It’s also critical for brands to be prominent on Search to capture the attention of the unbanked because they tend to have one brand in mind when they reach the Search bar.11

Once the unbanked find your brand, create a positive first impression of digital banking by having an app that is simple to use. Ensure that the app onboarding process is smooth and intuitive so that they find it easy to get started and are motivated to continue.

The underbanked are looking for reassurance before adopting new products

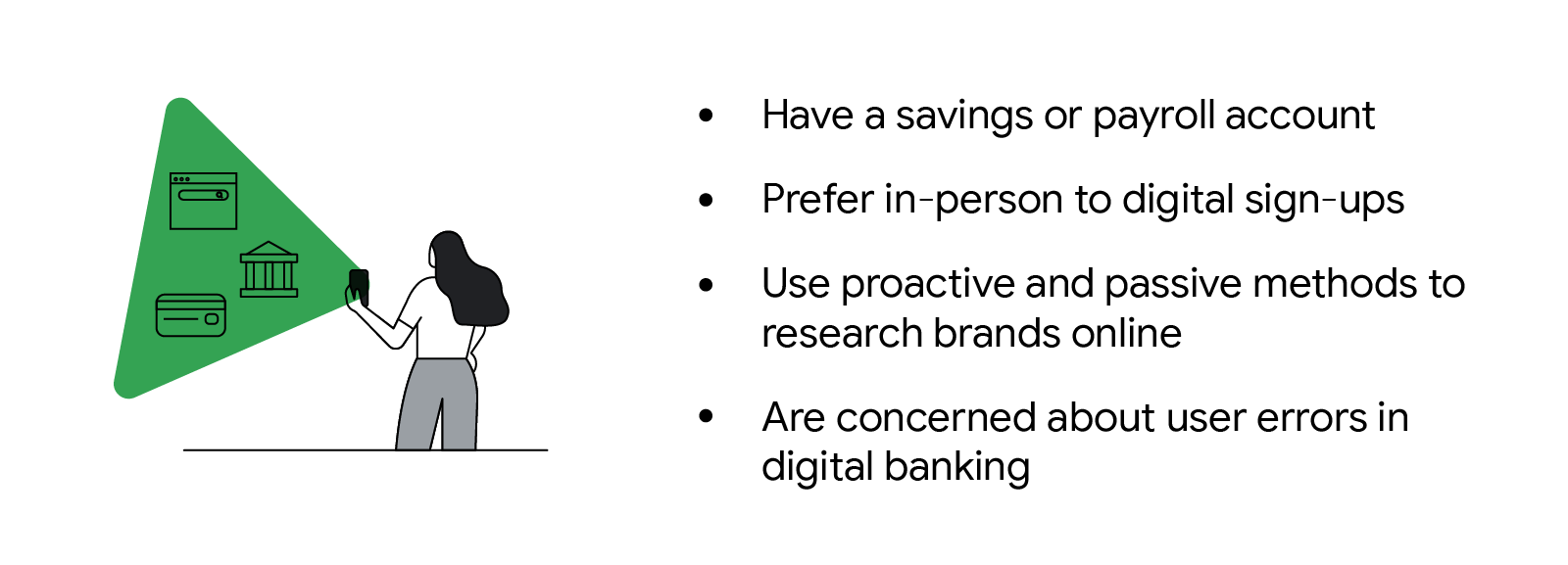

Our study found that the underbanked are generally older, less affluent, and share financial responsibilities at home.12 They own a savings or payroll account, but aren't as digitally savvy as the banked, so they are not as confident about using digital finance tools.13 This explains why the underbanked are more likely to sign up for a service in-person because they can get personalized answers and help on the spot.14

Financial behavior traits of Filipinos in the underbanked segment

While the underbanked are proactive in their research, they’re equally influenced by social media, online advertising, and friends and family.15 They usually have multiple brands in mind when researching, likely because they’re looking for the right brand to guide them in their finance journey.16 To engage the underbanked, brands need to provide assurance throughout their finance journey, starting with Search.

The underbanked have safety concerns about digital finance services, especially around identity theft, and they often use Search to look up reviews or to check for scams and frauds.17 So be proactive about educating them on financial safety topics like identifying scams and protecting their digital identity.

Brands can also deliver alerts and notifications at key points in people’s transactions to provide the underbanked with peace of mind. Among the underbanked, 55% believe that digital banking is risky due to user error,18 such as entering the wrong account number and sending money to a stranger. To avoid such errors, they seek real-time transfers, transaction history access, and constant reassurance through SMS notifications.19

The underbanked need to feel confident to truly embrace digital finance. Brands can play a key role by guiding them each step of the way, from providing the right cues in digital transactions to educating them about financial safety.

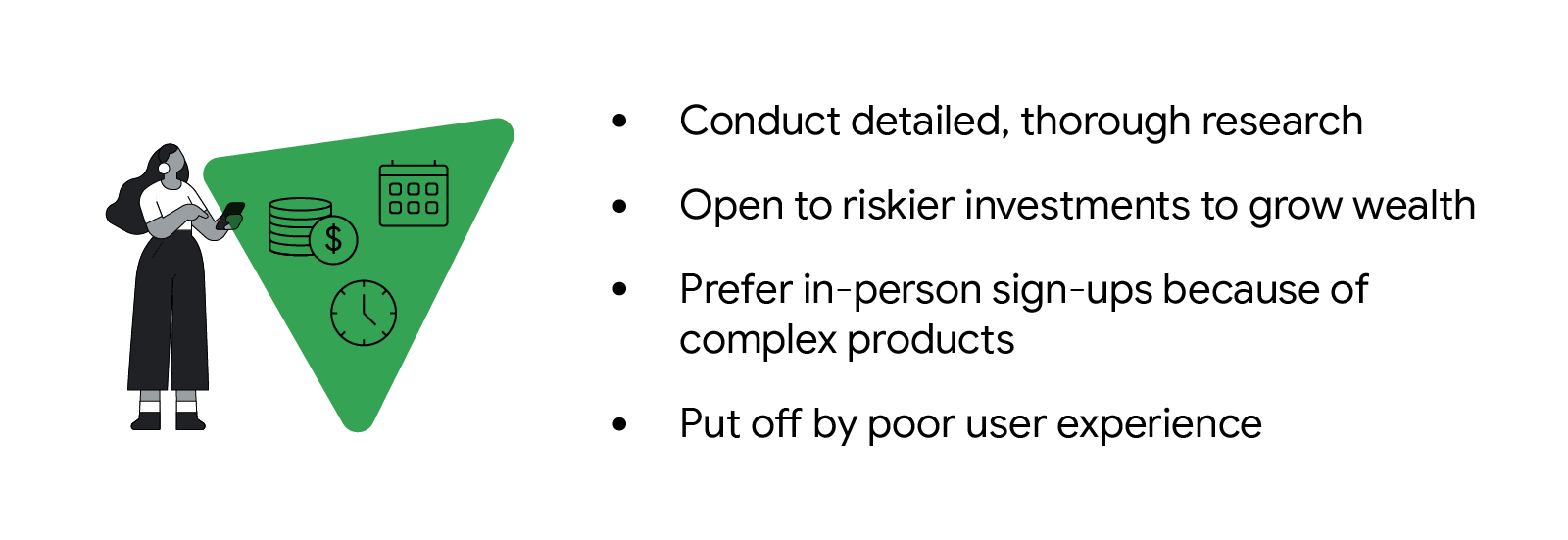

The banked are digitally savvy and actively researching ways to grow wealth

The array of digital finance offerings in the market and the widely available information about them have fueled a desire for financial advancement among the banked.20 People in this group look for financial growth via complex, riskier investments, and on average, they manage five to six financial products.21

Financial behavior traits of Filipinos in the banked segment

The banked are also thorough and detailed in their research. Scrolling through videos and brand websites and seeking advice from family, friends, and financial experts, they average 7.2 touchpoints in their research.22 Brands can meaningfully reach this segment by showing up on Search with relevant information. For instance, when people in this group are researching a new car, financial ads that surface information about car loans will be useful to them.

They’re also open to various financial products, regardless of brand, as long as it brings them closer to their financial goal. Given that they may not stick with one brand in their finance journey, building brand loyalty with this segment can be a challenge, but it is not impossible if you provide them with financial results and a quality experience.

Poor user experience is a deal-breaker for the banked, so continually optimize your websites and apps.23 Be sure to deliver a seamless online-to-offline experience for these customers. The offline experience is especially important to the banked, who prefer in-person sign-ups because of the complex nature of the products they’re interested in and the additional support they may require.24

As the unbanked, underbanked, and banked in the Philippines embark on new digital finance journeys, brands are presented with a never-before opportunity to cater to emerging needs at scale. Brands can support Filipinos on this new journey by building their trust and confidence every step of the way, from their search process to their user experience of digital finance tools.